William asked me to expand in this blog on an entry he made May 2 with Robbie Wright and I commenting.

We should not view the competition as other FI’s but as ourselves lacking the development of a website as a relationship deepening tool.

- Maybe it isn’t only the website but the products that could be an integral part of the website. This is important in the DIY process.

- This is constant (because nothing will stand still on the web) as we leap frog to better technologies. That is the development domain we now live in.

- This pushes us to a re-invention of product and service needs in attempt to marry relationship and technologies. It needs to be a virtual human touch or virtual human experience (VHE).

- Can we create these products and services? YES, but only if we are constantly vigilant to keep tech development along with a VHE. Without this we become a common process, a commodity.

- New products by the nature of being new will create a uniqueness which can be identified as personal (who else is using this?)

Advantage us, the credit unions!

Just by our nature and history we have a sound base on which to build. Our brick and mortar can only serve to enhance, in the member’s mind, our personal and ongoing relationship as it comes to product and service. These are the elements to clone in the VHE. As William pointed out and Robbie commented, e-tail experiences are to be as entertaining and amusing as personal experiences.

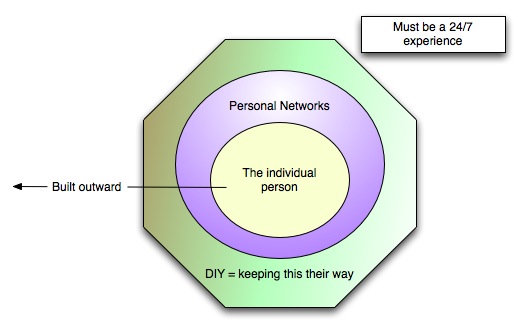

Products need to be built from the person out.

Start with the person, define their wants and needs. You should be able to create products fulfilling their needs invisibly by delivering it the way they want.

- 24/7

- DIY (customization). If a product has 12 variables to choose from, then the number of possible ways the product could be ‘developed’ or seen would be a factor of 12 = 78. With enough variables the end results could be close to unique for every member.

Incorporating the Products/Services into personal networks.

This is really new ground and will take some ingenuity on our part. Services that would be appreciated when viewed by others i.e. text messaging and would happen outside the realm of the branch could be one objective. Something that would touch that member in their own world which could be shared through common experience or through a shared virtual site would link to others to create dialogue and discussion. When we arrive here (The Wisdom of Crowds) the innovation and creation will take shape.

All this time the individual person keeps their products and services shaped their way (DIY).

Is this possible? Yes.

Where has it happened? If you have read this far you have some idea.

Where could this begin in earnest? Like minded CUs sharing these sentiments and discussion in a non-political atmosphere.

Well William I hope I have expanded enough. I think the time is coming when like minds need to discuss this around a personal event, like lunch.

Thanks Gene! I really appreciate the expanded answer. Your perspective is fascinating. The marrying of the product itself and the way it shows up on the website isn’t something I’ve ever really thought about before.

Yes, a lunch sounds essential. Can I selfishly ask if there’s a way we could meet without me having to drive to Abbotsford?

LikeLike

RE: “Maybe it isn’t only the website but the products that could be an integral part of the website.”

While you guys are lunching, just some thoughts from a radical, and you are hinting at it in your picture:

– I say forget about websites and product

– consider customer experience

– customers expect what?

Once you figure out the experience customers expect, you can think about the usual, people, process, technology stuff.

Product – my take: forget about it. It comes last. Banks have been product centric for ever, and that doesn’t work when you get into experiential design.

Lastly, Credit Unions have an ideal relationship with their customers to develop the emotive aspect of their customer experience. Work from there.

🙂

LikeLike

What does anyone expect from a FI? I would suggest the folowing.

Not having to wait in line. Take care of that first. No or minimal lineup are possible. Next before you do anything with their account (read transferring money) be sure you communicate with them first and foremost. Forget about automatic phone answering systems. Have a person answer the phone and when they ask for a balance be sure you can securely give it to them. When they come in to talk to someone about a loan let them come into the loans office now, not at a later date or time after making an appointment. The list goes on but the experience is just common sense. What do they expect? To be treated properly. Staff should treat member as they would like to be treated. The golden rule. From that base, and only from that base you need to move forward by tying in that crux to your products and services that need to operate outside the times you are open. 25 years ago you could only do banking when the doors opened. I don’t know what the figure is now but it might be 50%? of people’s banking is done on their own through some out of hours technology (for some it is even higher — I spoke with someone who hadn’t been in a bank branch for 3 years because of the lineups). Banks or whoever have not been able to produce product because the product can’t portray any extension of something other than themselves. Credit Unions have an opportunity from their base to develop or extend their products from who they are and will continue to be. For lack of an English word this would be the virtual human experience (VHE).

I agree 100% that before you do anything understand what the member expects, always exceeding those individual expectations and build on that. Don’t generalize but pay attention to each unique individual. The condtion of trust takes a lifetime to build.

Great comments!

LikeLike

I’m a big proponent of “the experience”, as Colin is, but for any company to be successful they need to apply their innovation and resources to both aspects of the business. I personally believe that the best product innovation comes direct from observing and dealing with your members/customers so the environment needs to help strengthen the feedback.

I believe Gene is correct, the VHE (virtual human experience) is a tremendous avenue to receive quality feedback. Wesabe is a wonderful example of this. They’ve been able to combine uber-sensitive data into a community forum and gather an amazing amount of insight. Not only does Wesabe listen to the direct feedback from their customers, but the data they can gather is extremely power in understand how people use their finances.

I’ve seen so many companies with terrible products because they don’t listen to end user feedback. It might be the next great thing, but if it can’t be used effectively and efficiently, it won’t.

Build the environment for your members, and you won’t have to worry about what latest technology to use or what your next product will be. You’re members will tell you.

LikeLike

Not to grossly oversimplify but at the end of the day we (banks/cu’s) are a lock and key protecting information that is stored in a data base. Ideally the user should be able to access and see the information presented in whatever way that would suit them best. We should not be an access barrier.

All products and technology can be commoditized… if you are do what I believe Gene is hinting at then the user becomes the architect of the product.. which due to the infinite permutations of possibility would be very difficult to replicate– aside from the actual process itself which potentially could be copied by other banks/CU’s.

This is actually not a new phenomenon, many companies these days are ‘handing the keys’ of product development over to the user creating environments with certain controls and parameters (regulations, legal requirements etc.) but allowing the user to do the rest. In a virtual world where we really aren’t ‘manufacturing’ anything except moving information bits around, this would be very plausible.

LikeLike

How do you do…

I am glad to find this forum !

fioricet http://fioricet–ok.blogspot.com

buy phentermine http://buy-1-phentermine.blogspot.com

The Author, you – genius…

cialis http://cialis-ok-1.blogspot.com

phentermine http://phentermine–mine.blogspot.com

Excellent site with fantastic references and reading…. well done indeed…!

payday loans http://payday-loans-ooo.blogspot.com

phentermine http://phentermine-electro.blogspot.com

I Will be back!

LikeLike